UncleJack….You’ve got some ‘spainin’ to do

One measure of my success in “preserving and protecting the Historic Neighborhoods” is the volume of my to-do list and the number of buyers that I’m working with. Providing you with 2 or 3 posts a day was always my goal and it’s easiest to accomplish when the to-do list is light. I’ve failed at various times due to personal health or family crisis events, but in general I’ve done pretty good. The last 2 weeks didn’t fare well in keeping that pace going. In general, I devote 2 or so hours a day to typing, editing, and picture taking to maintain the pace of the blog. There’s just not enough hours in each day, so something had to give.

So what have I been doing?

For one thing, I’m trying to find homes for a whole bunch of people. As you’ll see in the next post, that’s a challenge I didn’t think I’d be facing a few short months ago. Not that there aren’t buyers, which was the case a year ago – it’s that there’s no inventory. Shocking – I know. I think that “how can I have it both ways?” is going to be the theme of the rest of this post.

Buyers want nice livable houses that they can improve on during their upcoming years of ownership. “Regular sellers” don’t want to give away their houses. The bank homes generally aren’t livable, and most often aren’t being offered as accepting of FHA financing, which is how 95% of the non-investors are getting a loan. The regular seller’s had to compete against the banks. Now there’s little competition from the banks. In the next post down, I talk about some of the numbers.

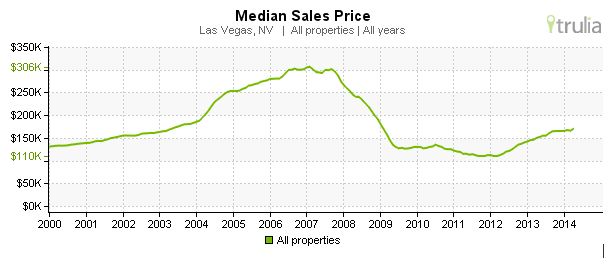

That means it’s time for the “regular sellers (who can, and want to) to start coming out from behind the blast barricade. I’ve said all along, and numerously, as well, that the Vintage Vegas neighborhoods are going to climb out of the hole faster and sooner than anywhere else in the valley. It’s starting to happen.

Appraisals:

And, I’ve been doing battle with the appraisers and the bank listing agents. They have a set of rules, and a whole bunch of bad habits. Many of them are lazy. Many of them are unwilling to look at the current “real” supply and demand for localized subsets of the market such as Vintage Vegas. Some are just collecting their fees and phoning it in. There’s a few I’ve dealt with recently who are actually doing their job and looking at something besides “how many square feet does it have”. I’m educating them as best I can that there’s a difference between “original footprint, well preserved and well loved vintage homes” and “abused, neglected and altered” vintage homes. And I’m trying to get across that some blocks, some streets, and some subdivisions are better and more desirable than others.

For examples, I’ve seen appraisals for homes in John S. Park, or Marycrest that have had homes east of Eastern Ave used as comparables. “But the square footage is the same!” No other explanation given. That’s despicable laziness.

I thought I was alone in my thinking, but Brian Wells covered the subject in an article in the Sun the other day, aptly titled: “Realtors complain about ‘low-ball’ appraisals”

Despite a 77 percent increase in existing home sales this year, some Realtors are complaining that low-ball appraisals are stifling sales.

First-time homebuyers and investors are leading the sales charge with home prices at their lowest in a decade, but Realtors contend that several appraisers are setting values that are much lower than they should be — and that those appraisals are killing sales.

Some call it an over reaction to the housing boom when some appraisers were accused of inflating prices on certain deals, prompting banks to lend more money than the property was worth. Appraisers contend they are setting prices based on what’s being paid in the market.

Mark Stark, owner of Prudential Americana, said he thinks appraisers are focusing too much on projecting what values will be instead of what they really are.

“The appraisers are being very conservative,” Stark said. “They are trying to cover themselves.”

What’s happening with appraisals has been felt the most in listings by homeowners who may, for example, have bought their home for $300,000 and are now selling it for $220,000, Stark said. If the appraisal came in at $205,000, that would force the seller to lower the price or the buyer would have to come up with $15,000 to make up the difference because the bank would loan only up to the appraised value, Stark said.

“The owner would rather tell them to drop dead than cut their price another $15,000,” Stark said. “I would say it is not causing us to lose all of these sales, but it is affecting 20 to 25 percent of the sales.”

About two-thirds of the existing home sales have been lender-owned properties.

Meetings, Meetings and More Meetings.

At the Foreclosure Crisis Town Hall Meeting the other night, County Commissioner and Realtor Susan Brager suggested that the appraisal rules need to be modified to not allow foreclosure and short sale transactions to be used as comparables to homes where the sellers AREN’T in trouble or desperate. RIGHT ON! I’m suggesting that the bank homes be divided into two tiers. Tier one is livable homes that would qualify for FHA/VA financing. NO INVESTORS ALLOWED TO BID. Tier Two is INVESTOR ONLY. Let them fight it out among themselves. I’ve had 4 instances in the last 2 months where the buyer I was representing actually made the highest bid on an FHA acceptable home, only to get shut out because the bank took the highest CASH OFFER, even though the first time buyer bid more.

As taxpayers we should be outraged that the banks and Fannie and Freddie are LEAVING MONEY ON THE TABLE for the sake of expedient, fast, all cash sales – after taking our tax money to make up for their losses!. I’ve had several hours recently of discussions on this subject with Dina Titus, Chris G. assorted brokers, REO listing agents, and their assorted staffs. Everyone agrees, but no one is listening.

Also at the Town Hall meeting, I had a conversation with Kenneth LoBene, the Director of the FHA Las Vegas Field office. I asked him about the “shadow inventory” that’s being intentionally withheld from the market. He told me that 100% of it is in the north and southwest of the valley, and is almost entirely made up of the 25 or more to an acre, 2 and 3 story “monopoly houses –that’s my term for them, not his.

Also at the Town Hall meeting, I had a conversation with Kenneth LoBene, the Director of the FHA Las Vegas Field office. I asked him about the “shadow inventory” that’s being intentionally withheld from the market. He told me that 100% of it is in the north and southwest of the valley, and is almost entirely made up of the 25 or more to an acre, 2 and 3 story “monopoly houses –that’s my term for them, not his.

You know the ones I mean. Most Vintage Vegas affectionados laugh about them all the time. They’re not releasing them, because there’s already a glut of them on the market, and the buyers, if given the choice they didn’t have 3 or 4 years ago, absolutely detest them. If you really want cheap newish housing and don’t care where it is, there’s some real bargains. I’m willing to bet that we’ll see whole neighborhoods of them get bulldozed one day soon.

You know the ones I mean. Most Vintage Vegas affectionados laugh about them all the time. They’re not releasing them, because there’s already a glut of them on the market, and the buyers, if given the choice they didn’t have 3 or 4 years ago, absolutely detest them. If you really want cheap newish housing and don’t care where it is, there’s some real bargains. I’m willing to bet that we’ll see whole neighborhoods of them get bulldozed one day soon.

So the “shadow” inventory that I thought was coming from the banks just isn’t there. There are a couple of dozen or so abandoned homes scattered around Vintage Vegas that are in the pipeline, and there may be a whole new wave of foreclosures caused by job loss, but that’s a story that hasn’t been written.

ANYWAY:

All I really set out to do was to tell you that I’ll try to get back onto my normal blogging schedule, in order to keep you amused, educated and informed. I ended up doing a rant instead. Wish me good luck!