The housing market is hot, but not in a bubble

Existing home sales came in at a whopping 6,850,000, beating estimates with the highest print since 2006. Days on market fell from 36 days to 21 days on a year-over-year basis. Cash buyers remain at a historically high level of 19%, the same as last year, while sales grew 26.6% year over year. We have done a lot running around with the existing home sales data to be up just 2.4% year to date.

Existing home sales came in at a whopping 6,850,000, beating estimates with the highest print since 2006. Days on market fell from 36 days to 21 days on a year-over-year basis. Cash buyers remain at a historically high level of 19%, the same as last year, while sales grew 26.6% year over year. We have done a lot running around with the existing home sales data to be up just 2.4% year to date.

The housing market is clearly hot.

While we celebrate these strong numbers, keep in mind these three points:

First, expect the data to moderate, so don’t freak out when we see the rate of growth cool down. A normal trend will eventually materialize. You may be told that future moderation indicates “cracks in the housing market, but don’t buy into it. I previously wrote that if we really saw cracks in the housing market, these are a few indicators to track and to beware of doom and gloom housing headlines.

Second, if the next existing home sales report misses expectations, you may be told that this is due to a lack of inventory. Don’t listen. Remember, lower inventory tends to go with higher sales — and higher sales mean folks are buying homes…therefore…I know you are following me here… there must be homes to buy.

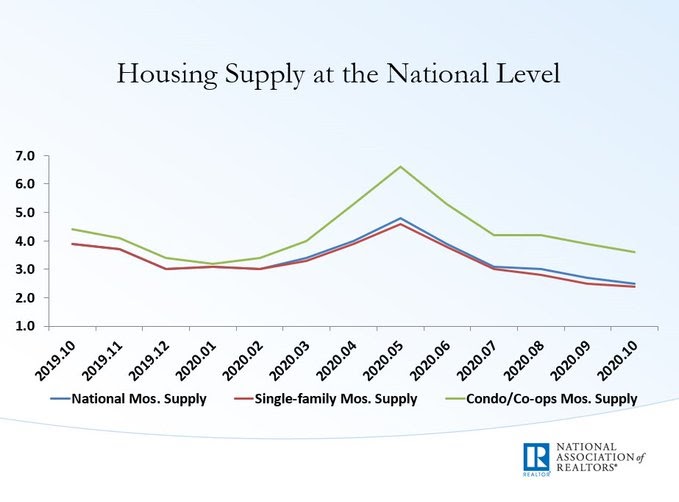

Unsold inventory sits at an all-time low 2.5-month supply at the current sales pace, down from 2.7 months in September and down from the 3.9-month figure recorded in October 2019. Inventory is tight, but it’s not non-existent. Tight inventory also encourages builders to create more inventory.

Lastly, we need to keep an eye on home prices. The increase of 15.5% year over year is a concern. My biggest fear for housing in the years 2020-2024 was not that home prices would crash by 30%-50%, as our bubble-boy friends have been telling us since 2012, but that real home prices might take off, creating an affordability issue for some buyers.

We have three exigent factors that could contribute to unhealthy price growth:

First, the years 2020-2024 have the best housing market demographics ever recorded in history. Second, housing tenure is currently at 10 years, double what it was from 1985 to 2007. People are staying in their homes longer. And third, mortgage rates will stay low during these five years of great demographics and long housing tenure. I expect mortgage rates to be below 5% the majority of this time unless some significant fiscal stimulus occurs when the economy is back on track after the COVID-19 crisis gets under control.

These recent reports concur with the strong mortgage purchase application data and pending home sales data we have had since May.

Again, expect these numbers to moderate — that is just part of the process for finding the trend — so don’t freak out. Before COVID-19, housing market data broke out for the first time in a long time. If you look back at the February data, we should have had total existing home sales of 5,710,000 -5,840,000. If we don’t hit those numbers, then COVID-19 took a little of the shine off of the demand, but this demand might just be pushed out to 2021.

Source: Housing Wire